404 - Not found

Sorry, we can’t find that page. It may have been moved or doesn’t exist.

Have questions? Need help? Contact us

Feel free to reach out during our business hours for assistance with estate planning, tax law, financial services, or other legal matters.

Call Us:

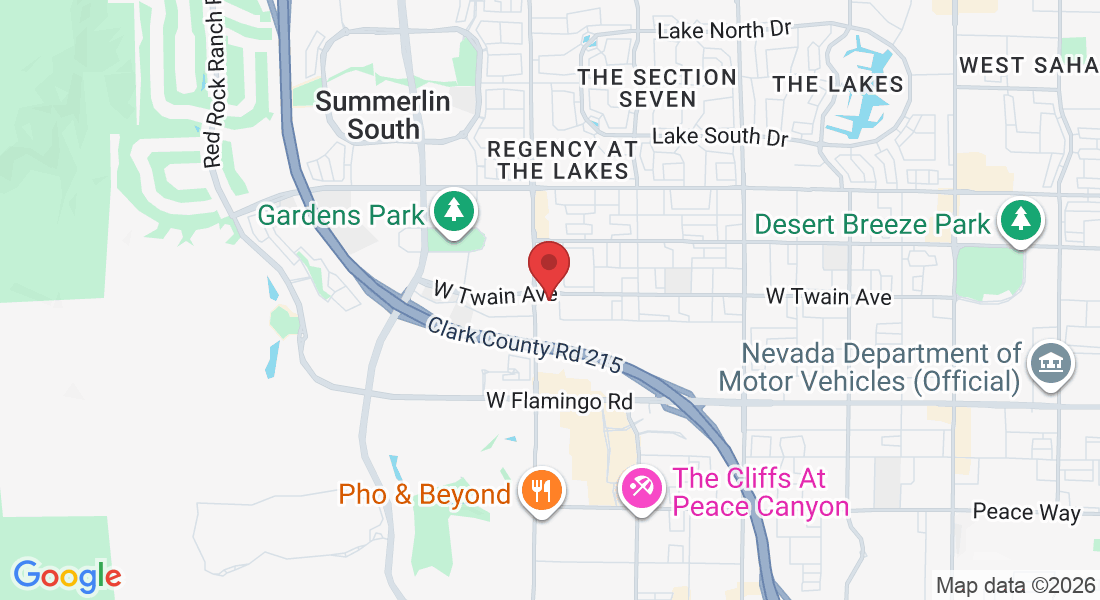

Visit Our Office:

10155 W. Twain Ave Ste 100 Las Vegas, NV 89147

Business Hours:

Monday - Friday: 8:00 AM - 5:00 PM

CPA Attorney, LLC is a one of a kind tax firm specializing in tax, financial services. We works with you to achieve the best possible outcome now and in the future.

Follow Us

© Copyright 2025 – CPA Attorney